What is Materiality?

Materiality is a term used to define what is important to the success of the business. We are focussed on Sustainability materiality, so aspects within Environment, Social and Governance (ESG) are considered.

The question to ask is “What ESG issues could affect the financial performance of the company or stakeholder decisions?”

These ESG issues should integrate into any existing materiality assessment, shaping the company’s short to long term strategy.

A successful Materiality Assessment will identify the key risks, opportunities and impacts relating to the sustainable operation of the businesses. An example of the material aspects of air pollution from burning fossil fuels, would be the associated costs of local climate regulations together with the impacts of CO2 and NOx in the atmosphere.

Using this example:

- the financial costs that climate regulations have on the business would be the financial materiality, and;

- the volume of CO2 and NOx released would be the impact materiality.

Combining these would be termed double materiality.

The decision of which approach to take depends on the purpose of the assessment. To comply with IFRS S1 and S2, a financial materiality (single) approach is required. Frameworks like the GRI and CDP break out themes that may/will be important to different stakeholder groups (investors, suppliers, regulators and staff) so should be reviewed at the start to ensure the best approach.

Materiality Assessment Process

The process begins by defining the boundary of the assessment. This includes determining which parts of the business, supply chain and value chain are covered. For many companies, this means considering core operations such as offices, warehouses, and logistics hubs, alongside key suppliers and customer relationships.

Setting these boundaries allows Scenario Analysis to be built into the process, which identifies risk under a range of possible future outcomes. Scenario Analysis helps organisations identify risks for different levels of global warming. Examples could be higher temperatures, floods, carbon pricing and biodiversity regulations under a low, medium or high climate change model.

Once the scope is defined, a comprehensive list of potential ESG topics is compiled. These topics are drawn from frameworks such as the ESRS, GRI, SASB. The long list is then refined to focus on topics most relevant to the organisation’s sector and activities.

Stakeholder engagement plays an essential role in this process. Consulting with a range of internal and external stakeholders helps ensure the assessment reflects multiple perspectives — from management and employees to customers, suppliers and investors. Through interviews, surveys or workshops, stakeholders are asked to consider the significance of each topic and how it affects them.

Each ESG topic is then evaluated using a consistent scoring framework. For environmental and social impacts, four factors are considered: scale, scope, irredeemable character, and likelihood. These capture how significant, widespread, permanent or probable the impact is. For financial materiality, two criteria are used: severity — the potential size of the financial effect — and likelihood — the probability of that effect occurring. Weightings can be applied where necessary to ensure that different types of impact are compared meaningfully.

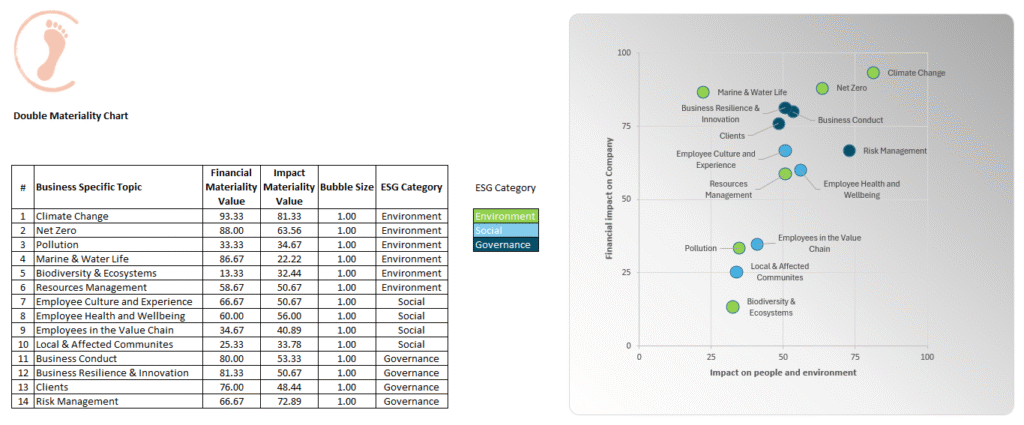

When the data, analysis and stakeholder feedback are combined, results are visualised in a double materiality matrix. Topics that appear in the upper-right quadrant — high in both dimensions — are considered the most material. Alongside the matrix, the findings should also be summarised in narrative form, explaining key risks, opportunities and dependencies.

Supply Chain vs Value Chain

While the two terms are often used interchangeably, they describe different parts of a company’s activity. The supply chain covers the operational flow of materials, goods and services that keep the business running — from sourcing and manufacturing through to delivery.

The value chain is broader, encompassing the entire lifecycle of how the organisation creates and delivers value, from product design and innovation to customer use and end-of-life. In sustainability reporting, assessing impacts across the value chain is essential because it captures both the upstream and downstream effects of operations, helping organisations understand where their most significant environmental and social impacts occur.

How is Materiality used in ESG reporting

The results from a double materiality assessment help to prioritise sustainability efforts, set measurable targets and align reporting with recognised standards. It’s clear to see then, how a materiality assessment would feed directly into the business strategy and be reflected through regular sustainability reporting and disclosures.

Conclusion

Double materiality provides a structured way to understand the two-way relationship between business performance and sustainability impact. When approached carefully, it moves beyond compliance to become a tool for meaningful insight, risk mitigation and action.

By combining stakeholder engagement, transparent methodology and a balanced evaluation of both ESG impact and financial significance, organisations can use materiality to strengthen their reporting, strategy and long-term sustainability performance.